Understanding the difference between taxable and nontaxable income is crucial for individuals and businesses alike. While taxable income is subject to federal and state taxes, nontaxable income is tax-free. This article by Naperville, IL, income tax planning advisors at Elder Hanson & Company, Ltd. will delve into the concept of nontaxable income, providing examples and explanations to help you navigate the complexities of your tax liability.

What Income Isn’t Taxable?

Nontaxable income is income exempt from federal income tax. While it may be reported on your federal income tax return, it doesn’t contribute to your tax liability. Some common examples of non-taxable income include gifts, inheritances, life insurance proceeds, and more. Despite these general guidelines, tax laws can be complex, and what is considered taxable income can vary based on individual circumstances. Keep in mind that while certain items may not be taxable on your federal income tax return they may be taxable on your state income tax return.

Taxable vs. Nontaxable Income

Before exploring the specific types of nontaxable income, it’s essential to clarify the distinction between taxable and nontaxable income.

Taxable income includes earnings or funds that are subject to federal or state income taxes. This encompasses:

- Wages

- Salaries

- Bonuses

- Commissions

- Self-employment income

- Rental income

- Investment income like dividends and capital gains

There are strategies available to reduce taxable income, whereas non-taxable income generally remains exempt from taxation under applicable tax laws.

Accurately differentiating between taxable and nontaxable income is vital for precise tax liability calculation. Errors in this area can lead to underpayment of taxes, which could result in penalties and interest.

20 Types of Nontaxable Income

Below is everything you should know about untaxed income. Understanding its types is crucial for accurately determining tax liabilities and maximizing after-tax income.

1. Disability Benefits

Disability benefits received from a qualified disability insurance policy due to a disabling injury or illness are generally nontaxable.

However, there are exceptions:

- Employer-paid premiums: If your employer paid the premiums for the disability insurance policy, a portion of the benefits may be taxable.

- Benefits exceeding pre-disability income: If your disability benefits exceed your after-tax earnings before the disability, the excess amount may be taxable.

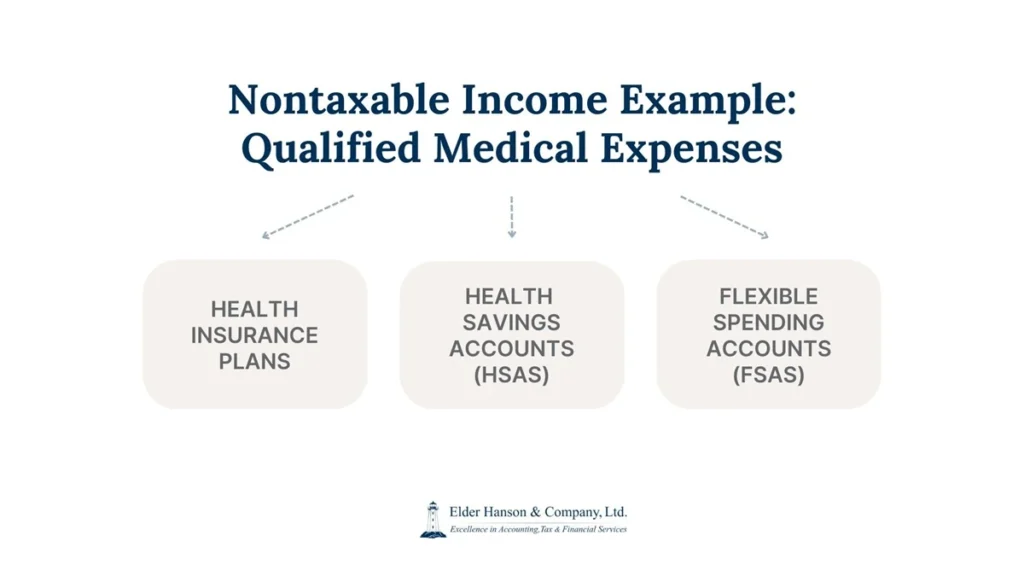

2. Qualified Medical Expenses

Reimbursements for qualified medical expenses are typically excluded from taxable income.

These reimbursements can come from various sources such as:

- Health insurance plans: Payments from health insurance for covered medical expenses are generally nontaxable.

- Health Savings Accounts (HSAs): Distributions from HSAs used to pay qualified medical expenses are tax-free.

- Flexible Spending Accounts (FSAs): Reimbursements from FSAs for eligible medical expenses are also tax-free.

It’s important to note that only qualified medical expenses are eligible for tax-free reimbursements. The IRS has specific guidelines for what qualifies as a medical expense.

3. Child Support Payments

Child support payments received are explicitly excluded from gross income and, therefore, aren’t subject to federal income tax. These payments are considered a matter of parental support and aren’t taxable to the receiving parent.

4. Fringe Benefits

While some fringe benefits provided by employers are taxable, others are not.

Common nontaxable fringe benefits include:

- Employer-provided health insurance: The cost of health insurance premiums paid by your employer is generally excluded from your taxable income.

- Life insurance: Group term life insurance coverage provided by your employer is generally tax-free up to specific limits.

- Accident and health plans: Employer-paid accident and health plans that provide benefits for injuries or sickness are typically nontaxable.

5. Life Insurance Proceeds

The death benefit from a life insurance policy is generally tax-free when paid to the designated beneficiaries.

However, there are exceptions:

- Policy surrenders: If the policyholder surrenders the life insurance policy for its cash value, any excess over the premiums paid may be subject to taxation.

- Interest income: Interest earned on policy dividends can be taxable.

6. Financial Gifts

Gifts are a common form of non-taxable income. However, there are specific rules and limitations to keep in mind:

- Annual gift tax exclusion: You can generally give up to a certain amount to as many individuals as you choose without incurring gift tax. The annual gift tax exclusion amount is adjusted annually for inflation. For 2025, the limit is $19,000 per recipient. Married couples can gift up to $38,000 combined.

- Lifetime gift tax exemption: While exceeding the annual gift tax exclusion doesn’t necessarily mean you owe gift tax due to the high lifetime estate and gift tax exemption, it does require filing a gift tax return.

- Charitable gifts: Donations to qualified charitable organizations are typically tax-deductible rather than non-taxable income. However, the income from these donations is generally not subject to tax.

- Employer gifts: Gifts from employers to employees, such as gift cards, are usually considered taxable income, with some exceptions for small, non-cash gifts.

It’s important to note that while the recipient generally doesn’t pay income tax on gifts, any income generated from those gifts (such as interest or dividends) may be subject to taxation.

7. Inheritances

Inheritances are generally not considered taxable income by the federal government. This includes inheritances of cash, property, or other assets.

However, keep the following in mind:

- Income from inherited assets: While the inheritance itself is not taxed, any income generated from inherited assets, such as dividends from stocks or rental income from property, is typically subject to income tax.

- State inheritance taxes: Although there is no federal inheritance tax, a few states do impose their own inheritance taxes including Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. However, many states have exemptions that exclude most estates from these taxes.

- Estate taxes: It’s crucial to distinguish between inheritance tax and estate tax. The estate tax is levied on the estate itself before distribution to heirs, while the inheritance tax is imposed on the recipients. The federal estate tax exemption is quite high, meaning most estates are exempt from this tax. However, several states impose their own estate taxes.

8. Scholarships

Scholarships are generally considered nontaxable income when used for qualified education expenses. These expenses typically include tuition, fees, books, and supplies.

However, there are exceptions:

- Taxable portions: If a scholarship covers room and board, or personal living expenses, that portion is generally taxable.

- Taxable stipends: Stipends paid to students in exchange for services, such as teaching or research assistantships, are often considered taxable income.

Don’t Tackle Taxes on Your Own

Effective tax planning can help you keep more of what you earn in Naperville, IL. Schedule a consultation and explore how Elder Hanson & Company, Ltd. can help you achieve your financial goals.

9. Worker’s Compensation Benefits

Worker’s compensation benefits are payments received by employees who experience work-related injuries or illnesses. These benefits are generally tax-free, regardless of the amount received. They typically cover medical expenses, lost wages, and disability payments.

10. Unemployment Compensation

Unemployment compensation is generally taxable. It’s considered regular income and is subject to federal income tax withholding. However, some states may also tax unemployment benefits. The amount of tax withheld depends on your filing status, income, and other factors.

11. Alimony Payments (for Divorce Decrees Finalized After 2018)

Alimony payments received under divorce agreements finalized after December 31, 2018, are not considered taxable income. This change was introduced by the Tax Cuts and Jobs Act. However, the alimony paid is no longer deductible for the payer.

12. Employer Contributions to Retirement Plans

Employer contributions to qualified retirement plans, such as 401(k)s, SEP IRAs, and SIMPLE IRAs, aren’t subject to federal income tax in the year they are contributed. These contributions grow tax-deferred within the retirement account. However, when you withdraw the money, it is generally taxable as ordinary income.

13. Municipal Bond Interest

Interest earned on municipal bonds is generally exempt from federal income tax. This makes them attractive investment options for many investors. However, it’s important to note that while exempt from federal taxes, interest on municipal bonds may still be subject to state and local income taxes, depending on your state of residence.

14. Long-Term Care Insurance Benefits

Long-term care insurance benefits are generally not subject to federal income tax. These benefits help cover the costs of long-term care services, such as nursing home care, assisted living, or in-home care. In some specific circumstances, such as when benefits exceed the cost of care, a portion might become taxable.

15. Social Security Benefits

A portion of Social Security benefits may be subject to federal income tax. The amount of taxable benefits depends on your combined income from other sources. The more you earn, the higher the percentage of your Social Security benefits that may be taxable. Some states also tax Social Security benefits.

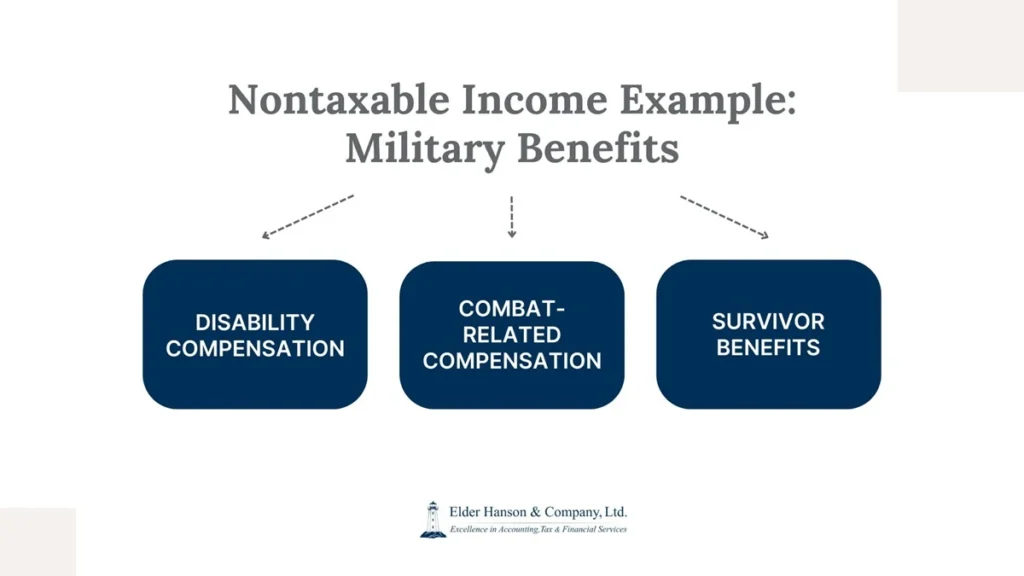

16. Certain Military Benefits

Some military benefits are exempt from federal income tax. These include:

- Disability compensation: Payments from the Department of Veterans Affairs for service-connected disabilities are generally tax-free.

- Combat-related compensation: Payments received for injuries or illnesses incurred while serving in combat zones are usually nontaxable.

- Survivor benefits: Certain survivor benefits provided to the families of deceased veterans may also be exempt from federal income tax.

17. Damage Awards for Physical Injury or Sickness

Compensatory damages received as a result of a lawsuit or settlement for physical injury or sickness are generally nontaxable. However, punitive damages and other types of awards may be subject to taxation.

18. Certain Government Assistance Programs

Benefits from government assistance programs are often nontaxable. Here are some examples:

- Supplemental Security Income (SSI): Payments from SSI, a needs-based program for low-income individuals and couples, are generally tax-free.

- Temporary Assistance for Needy Families (TANF): Cash assistance provided through TANF is also typically nontaxable.

19. Certain Foreign-Earned Income Exclusions

Individuals meeting specific requirements can exclude a portion of their foreign-earned income from U.S. taxes. This exclusion can help reduce the tax burden for U.S. citizens and residents working abroad.

20. Roth IRA Distributions

Understanding Roth IRA distributions is crucial for effective income tax planning. Qualified distributions from Roth IRAs can offer significant tax advantages. To qualify for tax-free withdrawals, you must meet specific age and holding period requirements:

- Age: You must be at least 59 ½ years old.

- Holding period: Your Roth IRA account must have been open for at least five tax years. This five-year period begins with the tax year in which you made your first contribution to the Roth IRA.

If both these conditions are satisfied, you can withdraw your contributions and earnings from the Roth IRA without incurring federal income tax or the early withdrawal penalty.

Important notes:

- Early withdrawals: Withdrawing funds before age 59 1/2 or before the five-year holding period generally results in taxes and a 10% early withdrawal penalty. There are, however, exceptions to the penalty, such as for first-time homebuyers, qualified higher education expenses, and certain disability cases.

- Roth IRA conversions: If you converted a traditional IRA to a Roth IRA, the five-year clock for tax-free withdrawals starts from the conversion date, not the original contribution date.

Importance of Tax Planning: Reach Out to Tax Advisors Today

By recognizing and maximizing nontaxable income sources, individuals and businesses can potentially reduce their overall tax liability.

Always remember that tax laws are complex and subject to change. To make sure you achieve optimal tax outcomes, you should consult with qualified tax professionals who can answer your questions and guide you in the right direction.

A comprehensive tax planning strategy can help you minimize your tax burden and protect your financial well-being. Get in touch with Elder Hanson & Company, Ltd. to start building a tax plan tailored to your specific needs.

FAQ

Is Social Security non-taxable income?

No, Social Security income is generally not entirely non-taxable. A portion of your Social Security benefits, sometimes up to 85%, may be subject to federal income tax, depending on your overall income. The specific amount taxed depends on your filing status and other income sources.

Is inheritance money considered earned income?

No, inheritance money isn’t considered earned income. Earned income is typically from wages, salaries, or self-employment activities. Inheritance is a transfer of wealth and not income generated from work performed.

Is 401k non-taxable income?

Not exactly. Contributions to a regular 401k plan are made with pre-tax dollars, meaning they reduce your taxable income in the year you contribute. However, the money grows tax-deferred within the account. When you withdraw the funds during retirement, it’s generally considered taxable income.